Categories

Discover our Courses

Featured Pathways

More pathways

Banking Essentials - Part I

This pathway will walk us through the basics of banks, starting with some of the different types and their main functions, then starting to look at the regulation faced by the banks, both before and after the Global Financial Crisis.

Greenwashing

Greenwashing is the act of distributing false information about something being more environmentally friendly than it actually is.

More pathways

Ready to get started?

Plans & Membership

Find the right plan for you

Our Platform

Expert led content

+1,000 expert presented, on-demand video modules

Learning analytics

Keep track of learning progress with our comprehensive data

Interactive learning

Engage with our video hotspots and knowledge check-ins

Testing & certification

Gain CPD / CPE credits and professional certification

Managed learning

Build, scale and manage your organisation’s learning

Integrations

Connect Finance Unlocked to your current platform

Featured Content

More featured content

Tackling the Cost of Living Crisis

In this video, Max discusses the cost-of-living crisis currently enveloping the UK. He examines its impact on households as well as the overall economy.

CSR and Sustainability in Financial Services

In the first video of this two-part video series, Elisa introduces us to sustainability. She begins by looking at the difference between sustainability and corporate social responsibility, two terms that can be easily confused.

More featured content

Ready to get started?

Our Solutions

About Us

Testimonials

More testimonials

Mark Homans

Our sky high NPS following learner feedback speaks for itself - this platform has delivered a lot of value.

Fiona Quinn

Learning is accessible and the tool assists in the continued development of all our employees. It is a fantastic tool for our business!

More testimonials

Ready to get started?

Categories

Discover our Courses

Featured Pathways

More pathways

Banking Essentials - Part I

This pathway will walk us through the basics of banks, starting with some of the different types and their main functions, then starting to look at the regulation faced by the banks, both before and after the Global Financial Crisis.

Greenwashing

Greenwashing is the act of distributing false information about something being more environmentally friendly than it actually is.

More pathways

Ready to get started?

Plans & Membership

Find the right plan for you

Our Platform

Expert led content

+1,000 expert presented, on-demand video modules

Learning analytics

Keep track of learning progress with our comprehensive data

Interactive learning

Engage with our video hotspots and knowledge check-ins

Testing & certification

Gain CPD / CPE credits and professional certification

Managed learning

Build, scale and manage your organisation’s learning

Integrations

Connect Finance Unlocked to your current platform

Featured Content

More featured content

Tackling the Cost of Living Crisis

In this video, Max discusses the cost-of-living crisis currently enveloping the UK. He examines its impact on households as well as the overall economy.

CSR and Sustainability in Financial Services

In the first video of this two-part video series, Elisa introduces us to sustainability. She begins by looking at the difference between sustainability and corporate social responsibility, two terms that can be easily confused.

More featured content

Ready to get started?

Our Solutions

About Us

Testimonials

More testimonials

Mark Homans

Our sky high NPS following learner feedback speaks for itself - this platform has delivered a lot of value.

Fiona Quinn

Learning is accessible and the tool assists in the continued development of all our employees. It is a fantastic tool for our business!

More testimonials

Ready to get started?

Bank Capital Post 2008 Financial Crisis

January Carmalt

20 years: Research & banking

In this video, January examines the new regime for bank solvency subsequent to the financial crisis of 2008, taking a closer look at the ever evolving regulatory landscape for bank capital and hybrid instruments.

In this video, January examines the new regime for bank solvency subsequent to the financial crisis of 2008, taking a closer look at the ever evolving regulatory landscape for bank capital and hybrid instruments.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Bank Capital Post 2008 Financial Crisis

11 mins 17 secs

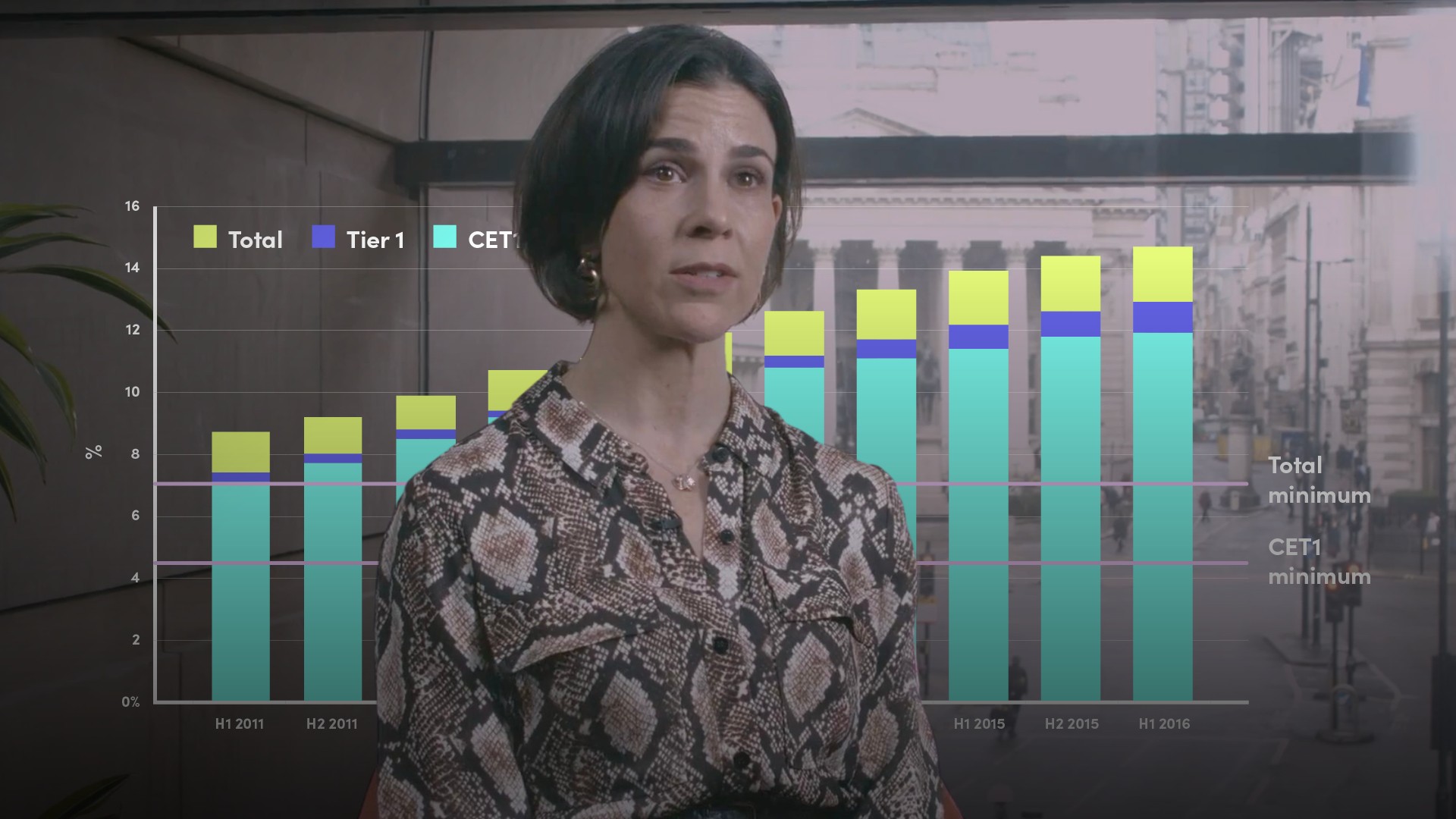

The 2008 global financial crisis led to material changes in the way bank capital is defined and calculated, and to more stringent capital adequacy regulations to ensure banks have sufficient capital to remain solvent without any need for taxpayer bail-outs. The specific trigger for the bankruptcy of Lehman Brothers in 2008 was an acute lack of liquidity i.e. an ability to refinance liabilities coming due and fund day-to-day activities. The acute liquidity crisis was directly precipitated by fears about the bank’s solvency.

Key learning objectives:

Define a bank’s basic capital structure today

Define bank solvency and understand why low solvency levels are a problem

Outline improvements that have been made to capital standards in recent years

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

What is bank solvency and why are low solvency levels a problem?

A bank’s solvency is a measure of its capital; put simply: assets minus liabilities. At the time of the global financial crisis, minimum capital requirements for banks were woefully inadequate. Many systemically-important banks operated very low solvency levels i.e. were woefully under-capitalised.

They had very slim capital buffers to absorb potential future losses from hundreds of billions in assets, and capital ratios were easy to manipulate using a variety of preference shares and structured hybrid securities. Old-style hybrid long-term securities (which had characteristics of both debt and equity) included now-defunct Upper Tier II bonds as well as a class of subordinated debt known as Lower Tier II bonds. The primary problem with these instruments was that they could only absorb losses in the event of a liquidation or when the bank had become a gone-concern.

What improvements have been made to capital standards in recent years?

Over the past decade governments, regulators and financial institutions themselves have made a number of game-changing strides to strengthen bank solvency levels: increasing minimum capital requirements and introducing stricter rules on what constitutes bank capital. Improvements include:

- The Basel III global capital standard, which outlined stricter regulations on capital and risk-weighted asset calculations

- An alphabet soup of new capital regulations, including Total Loss-Absorbing Capacity (TLAC) at a global level and its European iteration: the Minimum Requirement for Own Funds and Eligible Liabilities (MREL)

- Myriad government-led stress tests.

Bank capital structures today are much simpler. They ensure that institutions are adequately equipped to continue critical functions without threatening financial market stability. And there is a clear hierarchy of loss absorption and capital subordination that ensures the burden of losses in any financial crisis situation is transferred from taxpayers to stakeholders. This is referred to as a bail-in regime.

Define a bank’s basic capital structure today

- Going-concern capital

- Common Equity Tier 1: the bedrock layer of loss-absorbing capacity that includes shareholders’ equity and retained earnings (less goodwill, other intangibles and dividend distributions)

- Additional Tier 1 (AT1) a.k.a. contingent convertibles (CoCos): perpetual debt securities that absorb losses when a predetermined regulatory capital level is breached. Embedded contractual provisions impose either principal write-downs or conversion into equity

- Gone-concern capital

- Supplementary capital (Tier 2 capital): consists of revaluation reserves (i.e. the surplus created by the upward revaluation of an asset e.g. real estate owned), general loan loss provisions and subordinated Tier 2 bonds. Supplementary capital is senior to CET1 and AT1 but subordinate to other senior unsecured bondholders, senior preferred bondholders and deposits.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

January Carmalt

There are no available videos from "January Carmalt"