Categories

Discover our Courses

Featured Pathways

More pathways

Banking Essentials - Part I

This pathway will walk us through the basics of banks, starting with some of the different types and their main functions, then starting to look at the regulation faced by the banks, both before and after the Global Financial Crisis.

Greenwashing

Greenwashing is the act of distributing false information about something being more environmentally friendly than it actually is.

More pathways

Ready to get started?

Plans & Membership

Find the right plan for you

Our Platform

Expert led content

+1,000 expert presented, on-demand video modules

Learning analytics

Keep track of learning progress with our comprehensive data

Interactive learning

Engage with our video hotspots and knowledge check-ins

Testing & certification

Gain CPD / CPE credits and professional certification

Managed learning

Build, scale and manage your organisation’s learning

Integrations

Connect Finance Unlocked to your current platform

Featured Content

More featured content

Tackling the Cost of Living Crisis

In this video, Max discusses the cost-of-living crisis currently enveloping the UK. He examines its impact on households as well as the overall economy.

CSR and Sustainability in Financial Services

In the first video of this two-part video series, Elisa introduces us to sustainability. She begins by looking at the difference between sustainability and corporate social responsibility, two terms that can be easily confused.

More featured content

Ready to get started?

Our Solutions

About Us

Testimonials

More testimonials

Mark Homans

Our sky high NPS following learner feedback speaks for itself - this platform has delivered a lot of value.

Fiona Quinn

Learning is accessible and the tool assists in the continued development of all our employees. It is a fantastic tool for our business!

More testimonials

Ready to get started?

Categories

Discover our Courses

Featured Pathways

More pathways

Banking Essentials - Part I

This pathway will walk us through the basics of banks, starting with some of the different types and their main functions, then starting to look at the regulation faced by the banks, both before and after the Global Financial Crisis.

Greenwashing

Greenwashing is the act of distributing false information about something being more environmentally friendly than it actually is.

More pathways

Ready to get started?

Plans & Membership

Find the right plan for you

Our Platform

Expert led content

+1,000 expert presented, on-demand video modules

Learning analytics

Keep track of learning progress with our comprehensive data

Interactive learning

Engage with our video hotspots and knowledge check-ins

Testing & certification

Gain CPD / CPE credits and professional certification

Managed learning

Build, scale and manage your organisation’s learning

Integrations

Connect Finance Unlocked to your current platform

Featured Content

More featured content

Tackling the Cost of Living Crisis

In this video, Max discusses the cost-of-living crisis currently enveloping the UK. He examines its impact on households as well as the overall economy.

CSR and Sustainability in Financial Services

In the first video of this two-part video series, Elisa introduces us to sustainability. She begins by looking at the difference between sustainability and corporate social responsibility, two terms that can be easily confused.

More featured content

Ready to get started?

Our Solutions

About Us

Testimonials

More testimonials

Mark Homans

Our sky high NPS following learner feedback speaks for itself - this platform has delivered a lot of value.

Fiona Quinn

Learning is accessible and the tool assists in the continued development of all our employees. It is a fantastic tool for our business!

More testimonials

Ready to get started?

Mergers & Acquisitions (M&A) Valuation Methodologies II

Josephine Tan

20 years: M&A

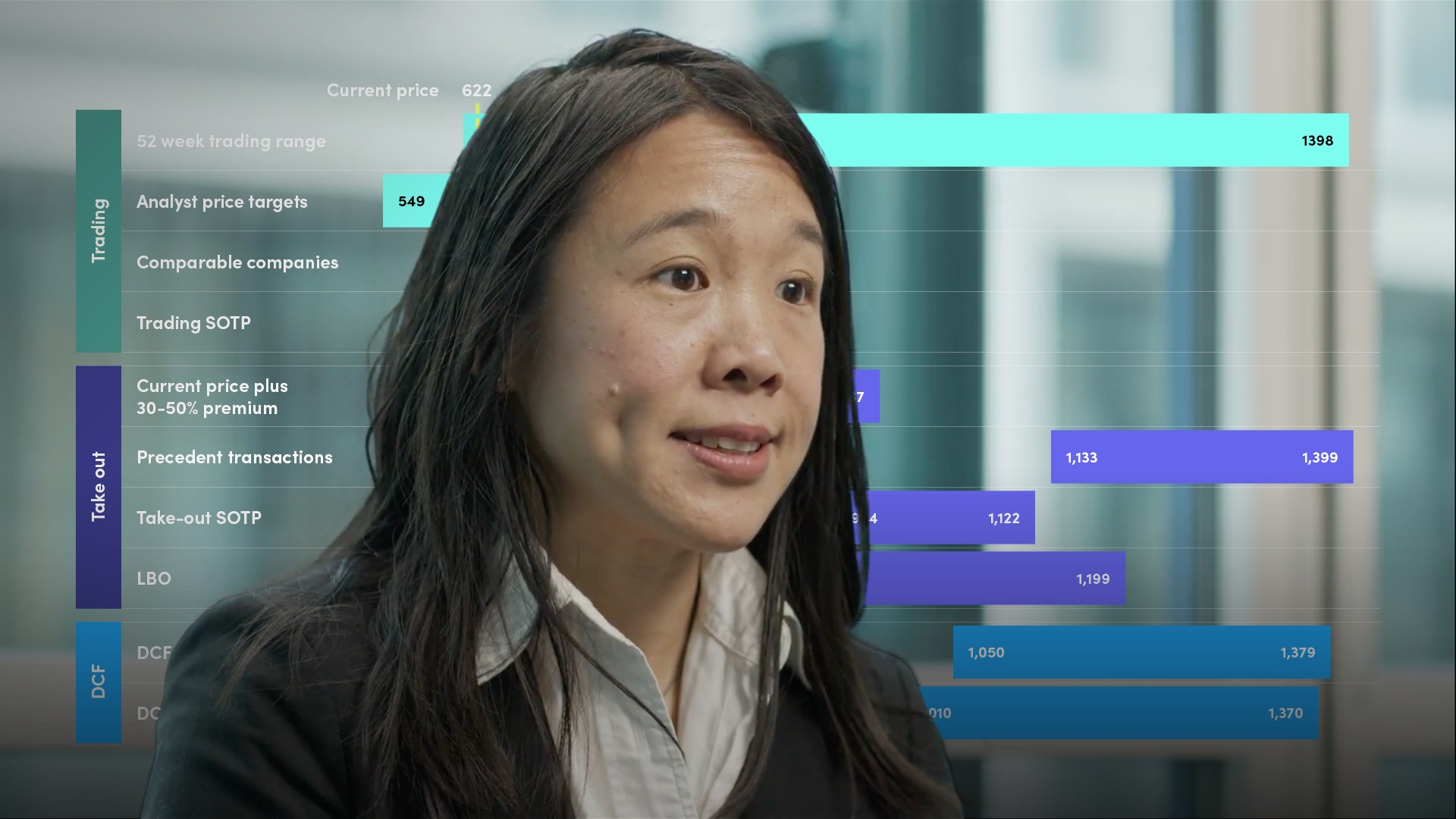

In the second part of Jo's video on valuations, she discusses various valuation methods, including precedent transaction multiples, discounted cashflows (DCF), leveraged buyouts (LBO) and sum-of-the parts.

In the second part of Jo's video on valuations, she discusses various valuation methods, including precedent transaction multiples, discounted cashflows (DCF), leveraged buyouts (LBO) and sum-of-the parts.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Mergers & Acquisitions (M&A) Valuation Methodologies II

8 mins 7 secs

Introducing the ‘precedent transaction multiples’, ‘discounted cash flow’, ‘leveraged buyout’ and ‘sum-of-the-parts’ methods to value companies or businesses.

Key learning objectives:

Understand the ‘precedent transaction multiples’ method, its pros and cons

Understand the discounted cashflow (DCF) valuation method and its limitations

Understand the Leveraged Buyout (LBO) valuation method, which companies it is best suited to and the key components of the analysis

Understand the sum-of-the-parts valuation method

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Explain the ‘precedent transaction multiples’ method, its pros and cons

The precedent transaction multiples valuation method (also known as “Comparable Acquisitions”) is a way to value a company or business using prices paid by acquirers rather than the traded market value. Relevant comparators are recent transactions in the same sector of a similar size with similar products and end markets operating in similar geographies. This facilitates a judgement as to the appropriate multiple ranges to apply to a company’s financial metrics to arrive at a valuation range. Pros- Usually based on publicly available information

- Valuation is not affected by temporary market conditions

- Multiples reflect actual transactions

- Public data is based on past transactions and may not be indicative of current market conditions

- Available information can be misleading because not all deal information is fully disclosed

- The multiples obtained for shortlisted transactions can sometimes vary widely

Explain the discounted cashflow (DCF) valuation method and its limitations

The DCF valuation method discounts projected future cash flows to arrive at a Net Present Value (NPV). It is useful for valuing businesses and assets that have limited comparables, no near-term cash flows or which have a known finite life. DCF valuations are based on a large number of assumptions and forecasts and are very sensitive to them, and can vary widely if assumptions are changed or incorrect.Explain the Leveraged Buyout valuation method, which companies it is best suited to and the key components of the analysis

LBO valuation analysis is used for companies or businesses from the perspective of a financial sponsor (private equity firm), which finances the acquisition with debt. There are five key parts of an LBO analysis:- The sources and use of funds for an acquisition – how much will be financed with debt vs. equity, and how will the funds be used (usually acquisition cost and debt repayment)

- Adjusting the balance sheet for new debt and equity

- Building a model that projects the cashflows for the company or business for the term of the investment and determining how much debt is paid down each year

- Calculating the exit value less debt that needs to be repaid

- Calculating the return after all the debt has been repaid. The maximum valuation at which a sponsor can acquire a company or business is set by target returns after paying off debt

Explain the Sum-Of-The-Parts valuation method

A sum-of-the parts valuation is a way of determining how much a company is worth if each of its underlying businesses or subsidiaries is valued separately and added up. A sum-of-the-parts valuation is useful for companies that have:- Well-defined business segments that are reported separately

- Holding companies or conglomerates with many different companies

- Companies with distinct assets

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Josephine Tan

There are no available videos from "Josephine Tan"