Key Details in a Bank's Annual Report

Ted Wainman

Chartered Accountant

In this video, Ted outlines the 5 key things to look for in a bank’s annual report. These include: how a bank funds its loan book; the relationship between the amount of equity and the total assets of the bank; the relationship between net interest income and other income; the amount being spent on costs as a proportion of total income; and whether it is adequately providing for non-performing loans.

In this video, Ted outlines the 5 key things to look for in a bank’s annual report. These include: how a bank funds its loan book; the relationship between the amount of equity and the total assets of the bank; the relationship between net interest income and other income; the amount being spent on costs as a proportion of total income; and whether it is adequately providing for non-performing loans.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Key Details in a Bank's Annual Report

9 mins 5 secs

Key learning objectives:

Identifying whether you are looking at the accounts of a commercial or investment bank

Ensuring that the costs are under control

Understand the importance of capital adequacy checks

Identifying the source of funds

Ensuring there is an adequate provision for ‘non-performing loans’

Overview:

The financial statements of a bank company are unlike those of any other organisation. Below are 5 key things to look for when confronted with the accounts of a bank.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

What is the difference between a commercial bank and an investment bank?

A commercial bank’s profit will primarily come from the difference between the rate paid on deposits and the rates charged on loans; this difference is known as the Net Interest Income. An investment bank will generate most of its profits from fees.

What is the biggest cost of a bank?

The largest cost of a bank is typically staff. Ensuring that these costs are covered is essential to profitability.

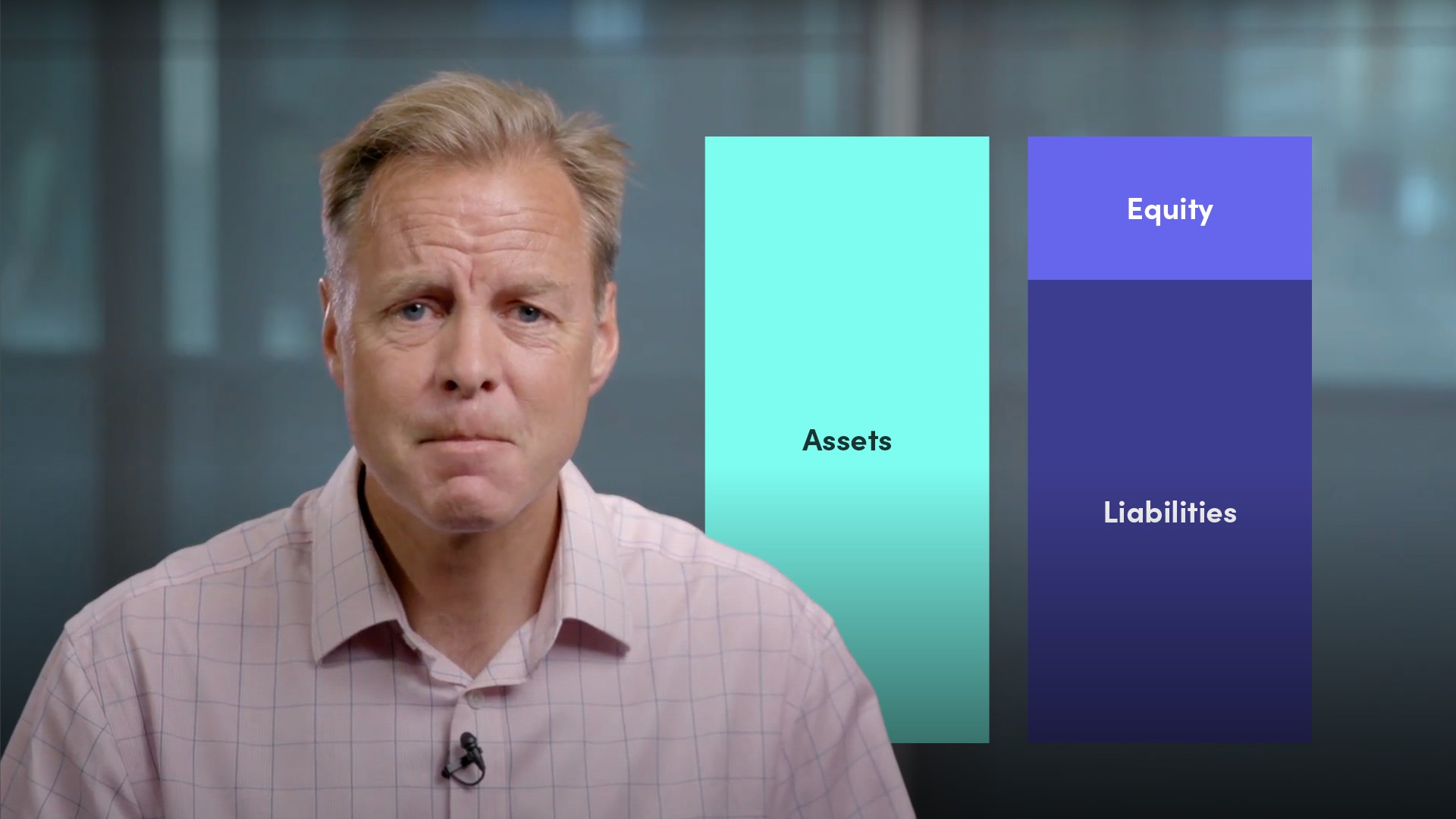

What is capital adequacy?

Capital adequacy essentially refers to the amount of shareholders’ funds that are available to absorb any losses and ensure that the bank does not default on depositors.

Where do banks get their funds?

Commercial banks are primarily funded through deposits with additional funds gained from issuing bonds. A third source of funding is inter-bank lending, but should not make up a material proportion of the overall funding model.

How do banks treat non-performing loans?

Statistically not all loans will be repaid. From missed interest payments to borrowers who have declared bankruptcy, a bank must monitor its loan book and ensure that the provisions for losses on loans are adequate.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Ted Wainman

There are no available Videos from "Ted Wainman"