Yield Curves in the Bond Market

Lindsey Matthews

30 years: Risk management & derivatives trading

Generally yield curves are built for a specific currency and for a specific issuer. In this video, Lindsey discusses LIBOR curves, the technical details behind building a curve and how this information applies to real curves.

Generally yield curves are built for a specific currency and for a specific issuer. In this video, Lindsey discusses LIBOR curves, the technical details behind building a curve and how this information applies to real curves.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Yield Curves in the Bond Market

17 mins 20 secs

Key learning objectives:

Identify the different types of yield curves

Understand the use of a yield curve

Recognise how to build a curve and its practical application

Overview:

Yield curves are highly important in fixed income. They allow an investor to value bonds and other instruments in order to identify a potential mispricing. Building a yield curve requires an understanding of forward rates and future expectations.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

What is a Yield Curve, and what are some examples?

Generally yield curves are built for a specific currency and for a specific issuer. In each case the curve is a set of rates or yields, by maturity, for a given currency and credit quality.

Examples would include:

- USD-US Treasury

- EUR-Bundesrepublik Deutschland

- GBP-VODAFONE-Senior debt

- USD-Corporate-Double A rated

- EUR-Italian-Banks

- EUR-Italian-Banks-BBB

When may Yield Curves be useful?

Building and analysing these curves each day, or even more frequently, is key for those operating in the fixed income markets. They provide an insight into where the market is trading, how it is moving, and what market expectations are. They also help investors to spot bonds that may be mispriced – rich or cheap, relative to the curve. As we have already seen, bond prices depend on their coupons and maturities and so are not directly comparable. It is their yields that are comparable, and so yield curves are used to analyse investment opportunities.

How is the LIBOR curve derived?

One key to this process is another curve quality that is commonly built, which is the LIBOR curve. These are built from instruments which reference the LIBOR index rate. The LIBOR rate is a polled rate which is published daily and is based on asking a group of banks the rates at which they would be prepared to lend money to each other, for various maturities, from overnight and 1 week, through 1, 3 and 6 months, all the way up to 1 year.

What are the LIBOR instruments?

- Deposit rates – the LIBOR rates themselves, based on polling banks for the rates they will lend to each other at, and therefore, giving an indication of rates for borrowing money

- LIBOR futures and FRAs (or forward rate agreements): allow users to trade where LIBOR rates will be in the future, and which are often used for hedging interest rate exposure, for altering rate exposure to meet a target, or for actually expressing a view on where rates are expected to be at some point in the future

- Interest rate swaps: allow users to trade the longer term level of LIBOR rates, for similar reasons as for futures

What are the uses of a LIBOR curve?

- They can be used to give an indication of the market level – as a benchmark curve

- They may be built as a reference – for example to compare where corporate bond yields are trading against the LIBOR or swap rates

- They may be built in order to price, value and risk manage books of interest rate derivatives – swaps, futures, FRAs

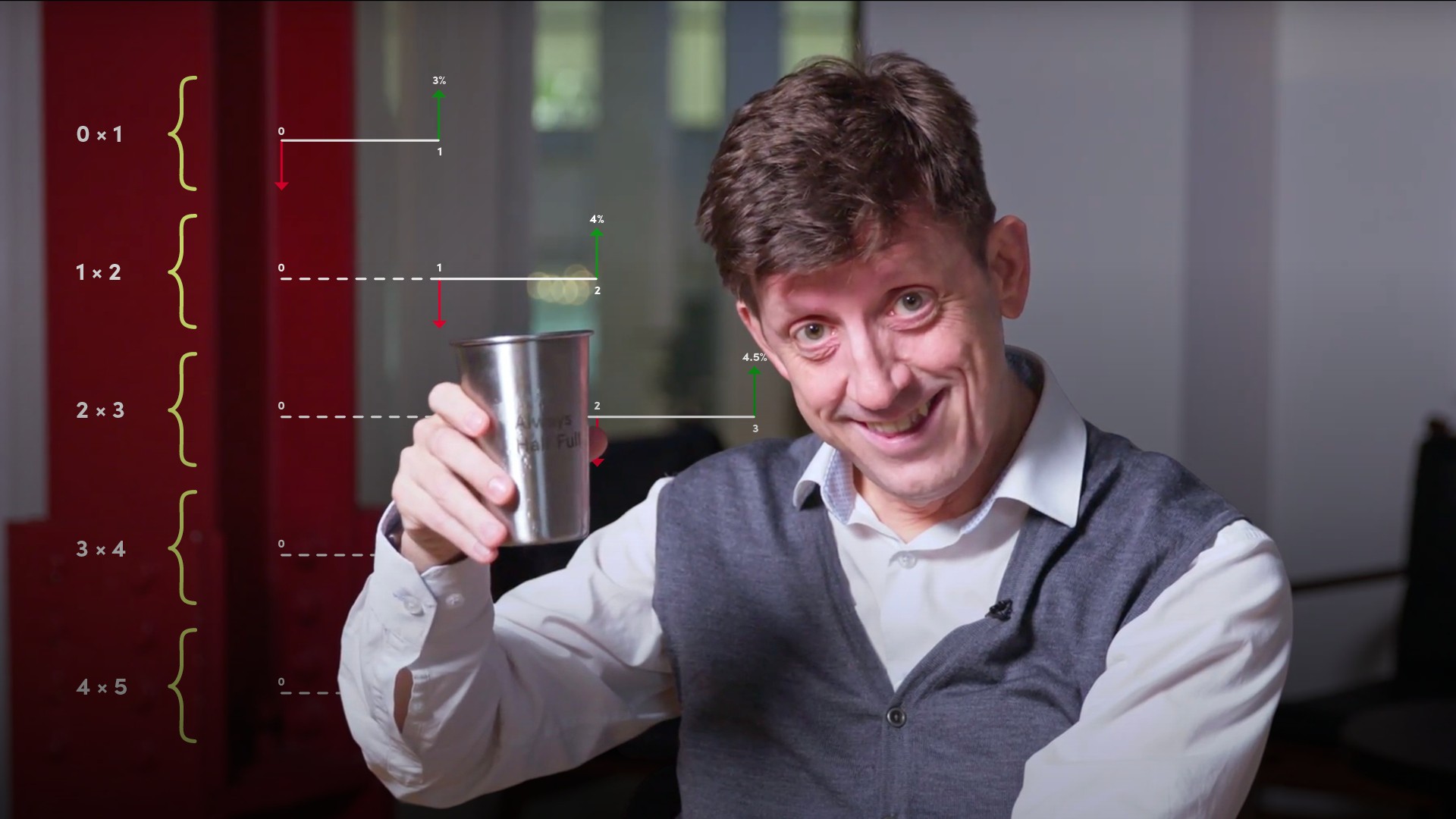

Why must we be careful when Curve Building?

When building curves, such as the bond curves or LIBOR curves we have just looked at, there are some technical details which mean we cannot just draw a line between all the yields and call that the yield curve. To do this is, at best, an intentional over-simplification, and at worst, a mistake that has caused millions of dollars of losses in the past.

Please reference the video for an in depth example of building a yield curve.

What does this mean for real curves?

Going back to our real curves, a US treasury curve shows rates on 1mo, 3mo and 6mo Treasury bills, and then yields on 1yr through to 30yr bonds. The rates on bills were like the zero rates in the curve built in our example. The rates on bonds were more like the par yields we just built.

When we built the LIBOR curve we used deposits (Which are like the zero rates here), futures and FRAS (which are forward rate instruments) and swaps (which are like par yields). And now you see that we can convert between any one of these types of quotation, and any other, and so we can build a curve from any – or indeed all – of these instruments.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Lindsey Matthews

There are no available Videos from "Lindsey Matthews"