Pricing Euro Bonds

Nigel Owen

Debt Capital Markets Practitioner

In this second part of the series, Nigel explains how to price a Euro denominated bond for the theoretical issuer, XYZ Corporation, using the building blocks outlined in the previous video. In this example, XYZ issues an eight-year bond.

In this second part of the series, Nigel explains how to price a Euro denominated bond for the theoretical issuer, XYZ Corporation, using the building blocks outlined in the previous video. In this example, XYZ issues an eight-year bond.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Pricing Euro Bonds

7 mins 52 secs

Key learning objectives:

Understand how the bond yield is reflected in the bond price

Identify the convention used in the euro bond market for coupon payments

Understand how a bond’s yield to maturity is calculated in the euro bond market

Define Euribor and what is an interest-rate swap curve

Describe the coupon rounding convention in euros

Understand the day-count convention for euros and its uses

Overview:

A bond represents a series of cash-flows. Investors buying bonds acquire rights to receive those cash-flows at a series of dates – the interest payments during the life of the bond (the coupons) and return of the money at maturity (redemption). For new bonds, buyers and sellers need to agree a price and a yield (discount rate) to arrive at a present value, or price, at which they can transact. The yield is a component of the risk-free rate plus a risk premium (a credit spread). The choice of benchmark hinges on the currency of issue and the conventions that apply to bonds issued in that currency.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

What convention is used in the euro bond market for coupon payments?

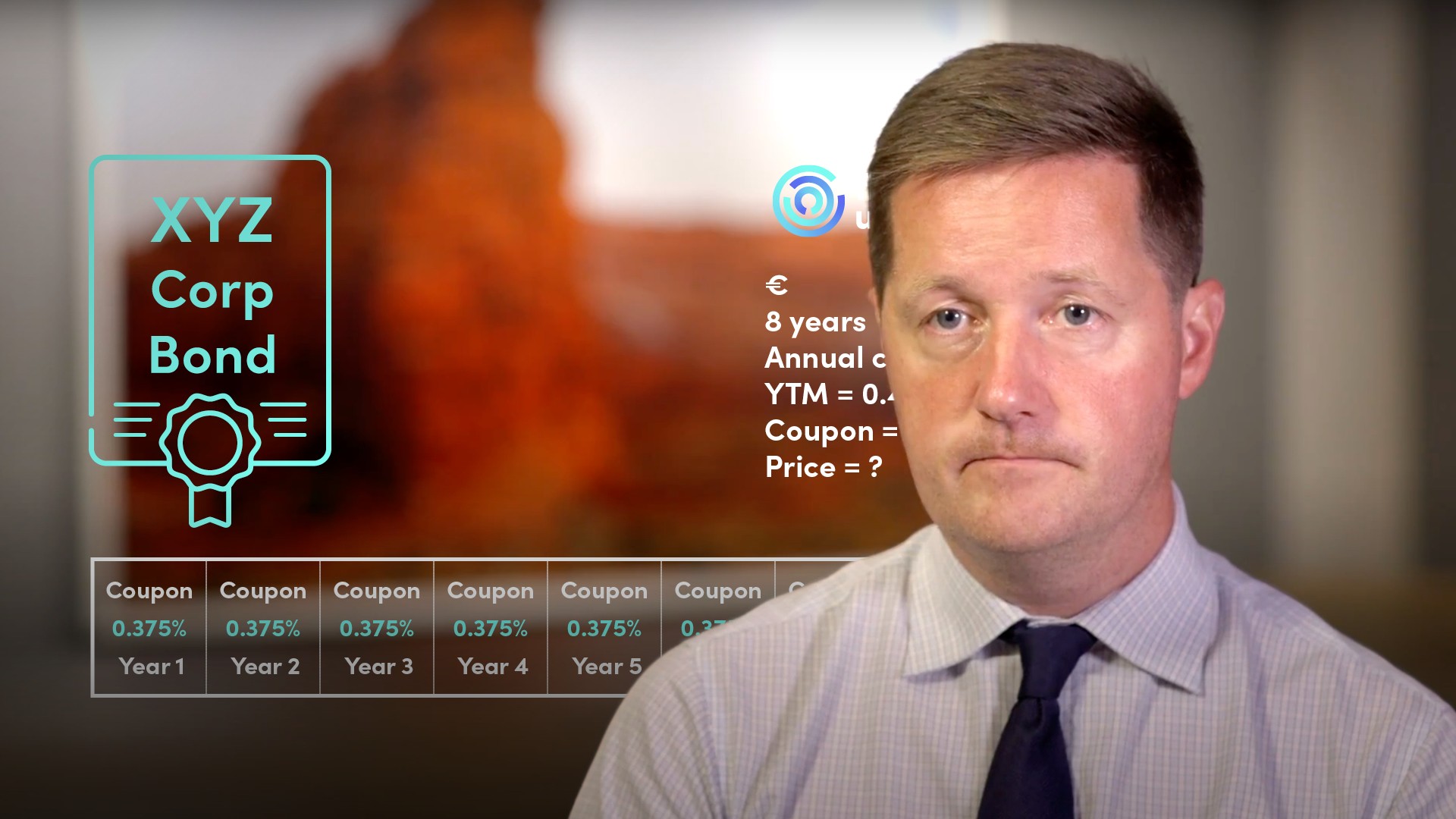

XYZ Corp has opted to issue an eight-year bond in euros. The company needs to decide the interest payments – or coupons – to which the bond’s eventual owners will be entitled. Bonds in euros are conventionally issued with annual coupons. Therefore the holder of a bond with a 2% coupon would receive that every 12 months.How is a bond’s yield to maturity calculated in the euro bond market?

The bond’s cash flows need to be discounted to calculate the yield of the bond. Calculating the yield on the bond has two components:

- The risk free rate. Every bond market has what is known as a benchmark rate, which is either the government bond curve or an established swap curve. Fixed-rate bonds in euros are priced using the so-called mid-swaps annual vs six-month Euribor curve. While bonds are priced using the swap curve, they are usually traded using the German Government bond curve as the benchmark. So XYZ Corp prices its eight-year bond against the eight-year mid-swap rate, which is -0.265%.

- The credit spread, which is the additional compensation investors demand to take on the extra risk of lending to a corporate issuer. This risk premium is quoted in basis points (i.e. 1/100s of a percentage point). The credit spread agreed with XYZ’s investors is 75 basis points or 0.75%. Adding that spread to the yield of the benchmark yield gives us a yield to maturity of 0.485% (0.75%-0.276%).

What is Euribor and what is an interest-rate swap curve?

Euribor is calculated using the average rates at which European banks lend to each other over short term maturities. It is not a risk free rate per se, but is still seen as a very low-risk rate. An interest-rate swap curve matches annual fixed-rate cash flows to six-month Euribor cashflows. Unlike the US dollar and sterling bond markets (which use government bonds to price bonds), the swap curve can provide a rate to match any chosen maturity date so there is no need for a convention to decide what swap rate to use. It also affords issuers in the euro market more flexibility to issue bonds with maturities that suit them, rather than having to conform to market conventions.What is the coupon rounding convention in euros?

With a yield to maturity of 0.485% and a redemption value of €100, assigning an issue price could be a really simple exercise: assigning a coupon of 0.485% and an issue price of 100 (or to use the jargon, par). The present value of a bond paying 0.485% coupon, discounted at a rate of 0.485% is par. However, convention dictates that bond coupons are rounded down to the nearest 1/8th of 1%. This means a coupon for XYZ of 0.375%.How is a bond yield reflected in bond price?

To reflect the 0.485% yield on a bond paying a 0.375% coupon, the issue price needs to be discounted. This discount can be calculated for every single cash-flow to derive a series of net present values, which can be added up to equal the appropriate issue price for the bond. For simplicity, a bond calculator can be used. Either way will tell you that to give investors a yield to maturity of 0.485%, XYZ’s bond should have an issue price of 99.139. To facilitate trading, the spread to the relevant benchmark Bund at the time of pricing also needs to be calculated. The benchmark eight-year Bund is quoted at a negative yield of -0.706%, giving XYZ’s bond a spread to the Bund of 1.186%, or 118.6 basis points.What is the day-count convention for euros and what is this used for?

To help future investors value and trade the bond during its life, day-count and business day conventions need to be borne in mind. As soon as XYZ’s bond is issued, it is free to trade, which means investors are free to buy and sell the bonds. The issuer’s obligation to pay coupons and redeem the bonds at maturity is limited to who owns the bonds at the time the obligations become due. Since coupons are usually only paid annually, it is typical in the euro market for each investor who sells bonds to have the buyer compensate them for interest accrued during the time they held the bond.

Day-count conventions set the framework for investors to calculate interest accrued when a bond has not been held for the full period of a coupon. In the euro market the convention is for accrued interest to be calculated on an Actual/Actual basis i.e. the calculation uses the actual number of days in the shortened period and the actual number of days in the full interest calculation period.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Nigel Owen

There are no available Videos from "Nigel Owen"