Quantitative Insurance Company Credit Rating Factors

Gurdip Dhami

Treasury and Ratings Expert

In the second video of his series on ‘Insurance company credit factors’, Gurdip describes the quantitative credit factors financial performance, asset quality and asset/ liability management. He also explains the number of profitability measures used by the rating agencies to assess financial performance.

In the second video of his series on ‘Insurance company credit factors’, Gurdip describes the quantitative credit factors financial performance, asset quality and asset/ liability management. He also explains the number of profitability measures used by the rating agencies to assess financial performance.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Quantitative Insurance Company Credit Rating Factors

18 mins 37 secs

Key learning objectives:

Understand the calculations for profitability

Identify asset quality on the basis of risk ratios

Understand asset and liability management

Overview:

Ratings agencies use a number of profitability measures to assess financial performance. S&P doesn't score profitability separately but includes it in its assessment of an insurers competitive position. A combined ratio above 100% means the company is paying out more to cover losses and expenses than it is receiving from premiums. Fitch states in its May 2020 rating report that Beazley PLC has low investment risk and a low level of risky assets. The Fitch calculated risk assets ratio for Beazley Plc for 2019 was 46% which equates to a AA score. Liquidity risk is the risk that an insurance company isn't able to pay financial obligations in full and on time. Most policies written by Non-Life companies are for one year, for example motor and property insurance. These insurers can plan and manage the liquidity risk more easily than for a Life insurer which may have liabilities up to 30 or 40 years in future. Fitch has a similar ratio for Life insurers called the Liquid Assets Ratio. The numerator is cash and short term invested assets, investment grade bonds, 50% of non-investment grade bonds/deposits, and publicly traded equities. The denominator is the policyholder reserves.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

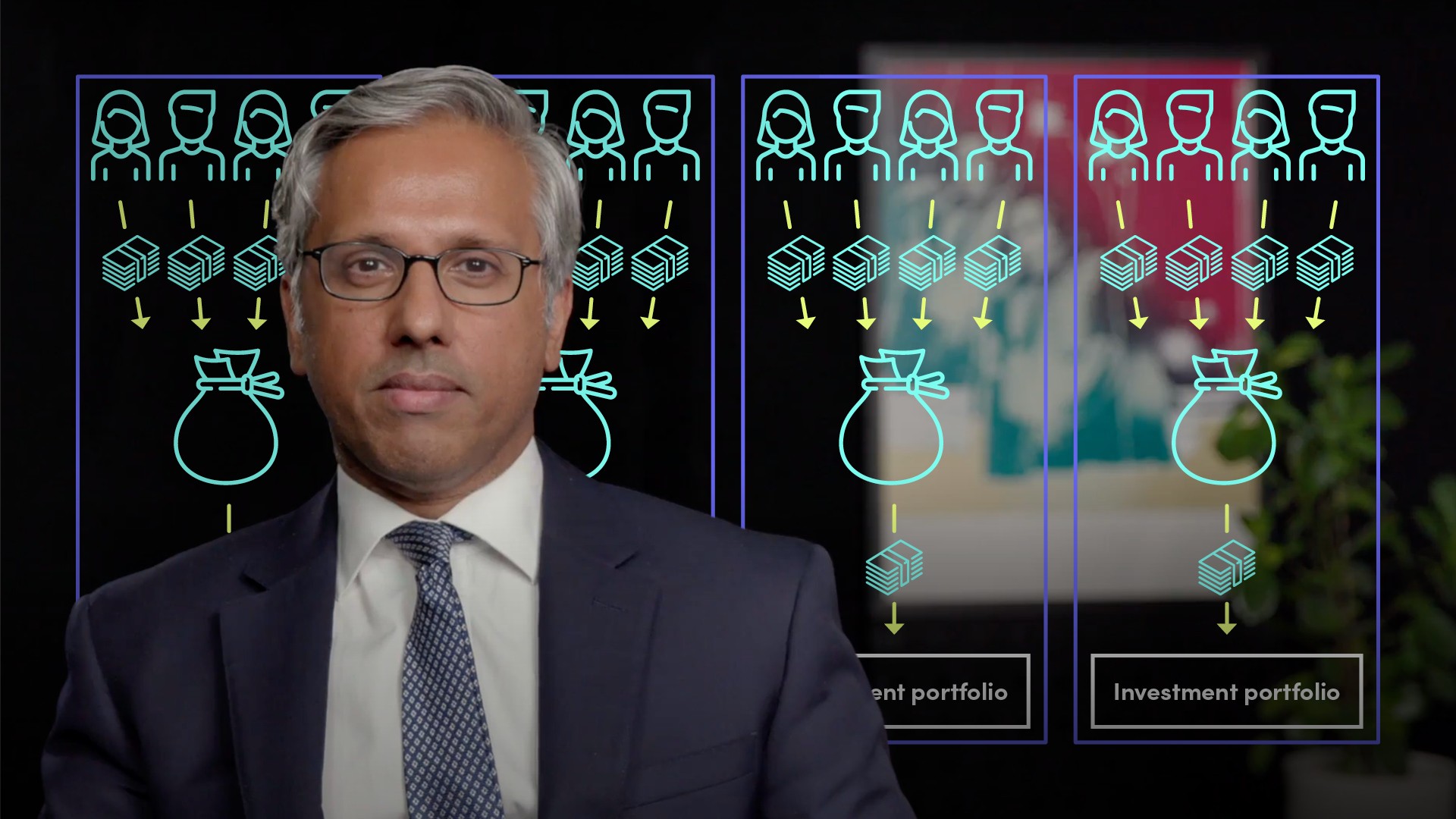

How is the profitability of a portfolio calculated?

Ratings agencies use a number of profitability measures to assess financial performance. Common profitability ratios for insurers include return on equity, return on capital and return on assets. For non-life insurers cost/income or margin measures are additionally used such as the return on revenue and the combined ratio. S&P doesn't score profitability separately but includes it in its assessment of an insurers competitive position. Fitch uses the average equity less minority interests and average assets in the denominator of the relevant ratios. The relative level of incurred losses indicates how well the insurer is underwriting its policies.

A combined ratio above 100% means the company is paying out more to cover losses and expenses than it is receiving from premiums. Fitch calculates and scores the combined ratio: for example, a combined ratio of 99% to 106% has a score of single A. S&P and Fitch will review the volatility of the profits qualitatively. An insurer which has more risky products and higher leverage would be expected to have higher profitability over time.

What are the criterias defining asset quality?

Insurance companies invest the premiums received by policyholders in various asset classes to earn an investment return. The directors of the insurance company manage the risks in the investment portfolio to optimise the risk and reward. Standard ratios include various types of "high risk" or "risky" asset ratios. Fitch defines risky assets as below investment-grade bonds, unaffiliated common stock and "other risky assets" Moody's defines high risk assets as those which are not investment- grade bonds or mortgage loans. The denominator in Fitch's risky asset ratio is equity.

In Moody's criteria, if the% of high risk assets relative to equity and loss absorbing capital is between 50% and 100% then the insurer is scored as single A. The exact details of the definitions and ratios are found in the criteria. Fitch states in its May 2020 rating report that Beazley PLC has low investment risk and a low level of risky assets. The Fitch calculated risk assets ratio for Beazley Plc for 2019 was 46% which equates to a AA score.

What is asset and liability management? Why is liquidity risk important?

Liquidity risk is the risk that an insurance company isn't able to pay financial obligations in full and on time. Life insurance companies have a greater focus on liquidity for life insurance companies than non-life companies due to their longer tail of business. Most policies written by Non-Life companies are for one year, for example motor and property insurance. These insurers can plan and manage the liquidity risk more easily than for a Life insurer which may have liabilities up to 30 or 40 years in future. Moody's standard liquidity ratio for life Insurance companies is liquid assets as a % of liquid liabilities. The ratio is calculated assuming a one year stress scenario. The main type of ratio that the agencies use to assess liquidity is to compare the current level of liquid assets to the potential outflow of cash due to policyholder claims and other obligations such as dividend and loan payments.

Moody's provides a score for the ratio: for example a ratio between 1.5X and 2X is given a score of single A. Fitch has a similar ratio for Life insurers called the Liquid Assets Ratio. The numerator is cash and short term invested assets, investment grade bonds, 50% of non-investment grade bonds/deposits, and publicly traded equities. The denominator is the policyholder reserves. Interest rate risk is potentially a large risk for life insurers given the long maturity of its liabilities. It is usually less of a concern for Non-Life insurers.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Gurdip Dhami

There are no available Videos from "Gurdip Dhami"