Required Return on Equity

Sarah Martin

Corporate Valuations Consultant

In this video, Sarah explores the required return on equity, a crucial input into the weighted average cost of capital (WACC). She explains how this is typically estimated using the capital asset pricing model (CAPM), and breaks down its key components: the risk-free rate, the market risk premium, and beta. She also highlights some of the practical issues that arise when applying this model.

In this video, Sarah explores the required return on equity, a crucial input into the weighted average cost of capital (WACC). She explains how this is typically estimated using the capital asset pricing model (CAPM), and breaks down its key components: the risk-free rate, the market risk premium, and beta. She also highlights some of the practical issues that arise when applying this model.

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Required Return on Equity

8 mins 38 secs

Key learning objectives:

Understand what is meant by the required return on equity

Learn how CAPM is used to estimate the return on equity

Understand the role of the risk-free rate, market risk premium, and beta

Identify the limitations and subjectivity in applying CAPM

Overview:

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

The required return on equity is the return investors expect for taking the risk of owning shares in a firm. Unlike debt, equity doesn’t guarantee a return so it is subjective and plays a major role in valuation via the WACC. The term is often used interchangeably with cost of equity, but “required return on equity” is more accurate since equity investors aren’t promised a fixed return.

Some investors use heuristics or expectations based on past experience. Others, particularly in corporate finance, use models like the capital asset pricing model (CAPM) to make this more systematic.

CAPM estimates the required return on equity by adding a risk premium to the risk-free rate. The formula is:

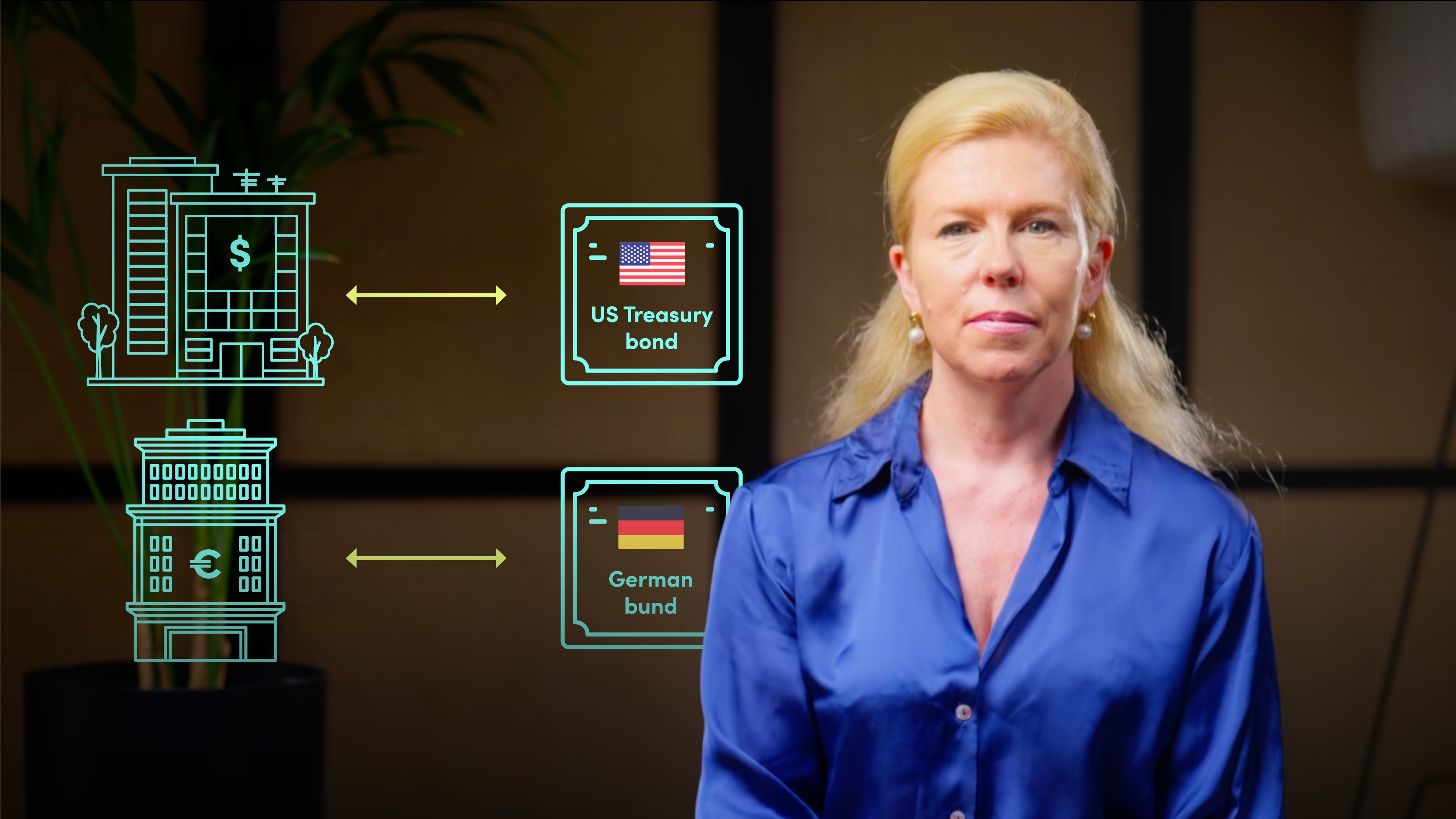

This is the yield on a default-free bond, like a US Treasury or German Bund. If valuing a firm in a country with lower credit ratings, a sovereign spread is added to reflect added risk. For example, valuing a Spanish company in euros would involve adding the spread of Spanish government debt over German Bunds.

This is the excess return investors expect from the market over and above the risk-free rate. It is typically calculated using long-term historical returns of equity markets, but results can vary depending on whether geometric or arithmetic averages are used.

Beta measures a stock’s sensitivity to overall market movements. A beta above 1 means the stock is more volatile than the market; below 1 means less volatile. Beta increases or decreases the required return based on the level of risk.

CAPM can be distorted by unreliable beta estimates, limited or non-existent market return data (especially in emerging markets), and differing interpretations of risk. Additionally, some investors see high beta as signalling upside potential (not necessarily more risk).

Subscribe to watch

Access this and all of the content on our platform by signing up for a 7-day free trial.

Sarah Martin

There are no available Videos from "Sarah Martin"